What is a Tax Shelter?

Introduction:

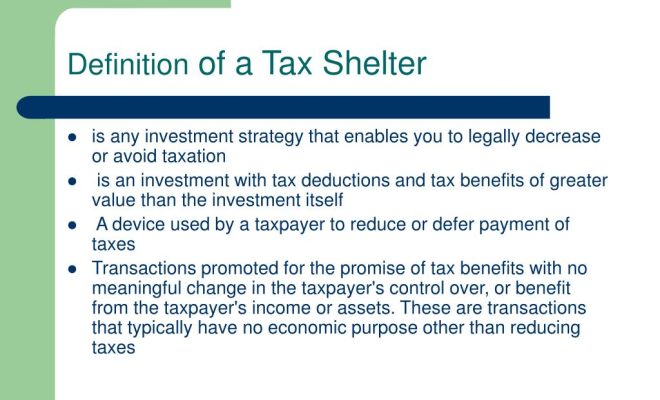

A tax shelter is a financial concept designed to help individuals and businesses reduce their taxable income, thereby paying less tax. Through various legal strategies, tax shelters safeguard assets and unlock extra financial benefits. In this article, we discuss the definition of a tax shelter, its purpose, and different types of tax shelters commonly used.

Defining Tax Shelters:

Simply put, a tax shelter is a method used to reduce taxable income, ultimately resulting in decreased taxes owed. It can be an investment or expense that either postpones or significantly lowers the amount of tax due on one’s income or earnings. The concept of tax shelters exists primarily for governments to incentivize specific behaviors, such as economic growth or environmental conservation.

Purpose and Benefits:

The main purpose of a tax shelter is to allow individuals and organizations to invest money without incurring high taxes. By doing so, they are encouraged to contribute towards prioritized areas for the economy, environment, or society. Using available deductions, credits, and other incentives helps taxpayers maximize their returns while promoting positive impacts in diverse sectors.

Types of Tax Shelters:

1. Retirement Accounts: One of the most common types of tax shelters comes in the form of retirement accounts such as IRAs (Individual Retirement Accounts) or 401(k)s. These accounts allow people to defer taxes on their income until they reach retirement age.

2. Real Estate: Real estate investments can provide numerous opportunities to create a tax shelter. For example, property owners can benefit from depreciation deductions, mortgage interest deductions, and certain exemptions when selling their main residence.

3. Business Expenses: For small business owners or self-employed individuals, expenses related to running their business can qualify as a tax shelter through deductions that reduce taxable income.

4. Health Savings Accounts (HSAs): HSAs are tax-advantaged savings accounts designed for people with high-deductible health plans (HDHPs). Contributions to an HSA are tax-deductible, and withdrawals for qualified medical expenses are tax-free.

5. Charitable Donations: Charitable giving can be used as a tax shelter when you donate cash, assets, or property to a qualified charitable organization. These donations can be deducted from your taxable income, reducing the total amount of taxes owed.

6. Municipal Bonds: Investing in municipal bonds issued by local, state, or federal governments can provide tax-exempt interest income. This means the interest generated from these investments is not subject to federal income tax and might also be exempt from state and local taxes.

Conclusion:

Tax shelters offer valuable financial opportunities to individuals and businesses looking to minimize their tax liabilities. It’s important to navigate these strategies with an understanding of their legal boundaries to avoid fines or penalties. Consulting a professional financial adviser or tax expert can prove immensely helpful in making the right decisions when utilizing tax shelters for personal or business use.